THE TICKER

President Trump, standing with Vice President Mike Pence and Treasury Secretary Steven Mnuchin, talks to reporters on Capitol Hill after meeting with Senate Republicans. (AP Photo/Susan Walsh)

President Trump’s promise to unveil an emergency stimulus package to address the economic fallout from coronavirus rallied stocks on Tuesday. One problem: The plan doesn’t exist.

The Trump administration and lawmakers from both parties are actually just in the earliest stages of talks toward a relief package. And there are serious divisions already emerging: The White House is pushing a payroll tax holiday that so far is getting a cold reception in Congress.

Trump is not helping his case by openly fixating on securing a political advantage. He told Senate Republicans at a closed-door lunch in the Capitol that he wants to suspend the payroll tax through the election, “so that taxes don’t go back up before voters decide whether to return him to office, according to three people familiar with the president’s remarks,” Bloomberg News’s Jennifer Jacobs reports.

The approach, of prioritizing his political wellbeing over the demands of the unfolding crisis, has characterized much of Trump’s coronavirus response to date. He has publicly contradicted the warnings of his own administration’s top public health officials to downplay the threat; misrepresented the federal government’s readiness to test for the virus; and urged Americans to buy stocks before sharp downturns in the market. Those decisions have further rattled investors eager for steady leadership out of Washington.

A day after Trump teased the rollout of “very dramatic” measures to shore up the economy — a preview that surprised his own economic team — his presentation Tuesday appeared haphazard, as “some of the ideas appear not to have been carefully vetted,” my colleagues Erica Werner, Josh Dawsey, Seung Min Kim and Bob Costa report. “One senator at Tuesday’s lunch meeting with Trump said the president also floated the idea of allowing Americans to delay filing their tax returns in April, reimbursing people or companies for sick leave and providing aid to the travel industry. But there were not precise plans on how any of these things would work.” (The WSJ reports the Trump administration is likely to extend the deadline though the mechanics of such a move remain unclear.)

And Trump’s pitch fell short on Capitol Hill, “as lawmakers of both parties said they preferred targeted measures to assist hourly workers and the battered travel industry,” the Wall Street Journal’s Andrew Restuccia, Andrew Duehren and Richard Rubin report.

Treasury Secretary Steven Mnuchin, following a half-hour meeting with House Speaker Nancy Pelosi (D-Calif.), declined to give the talks any formal weight. “I wouldn’t say it’s a negotiation. We’re having discussions about various different policies,” he said. Pelosi, for her part, “declined to say whether the two had made any progress on a deal,” per the WSJ.

The payroll tax holiday Trump’s pushing has a massive price tag – but administration officials failed to add any clarity at a White House news conference after the markets closed. Larry Kudlow, Trump’s top economic adviser, suggested that the growth a payroll tax holiday would unleash could make up for the estimated $900 billion hole it would blow in the budget just this year — a sum that the New York Times’s Jim Tankersley notes is greater than the price tag of both the 2008 Wall Street bailout and the 2009 stimulus package:

But Kudlow declined to get specific about how that math would work. “Let us put the proposal out in concrete details and flesh that out, and we’ll have much better answers,” he said.

Economists say a payroll tax holiday is exactly the wrong type of measure for this crisis. It skews its benefits toward higher-income earners while incentivizing people to work, when the aim of federal support should be to help those who need to stay at home.

The benefits wouldn’t concentrate on the most vulnerable workers – and would be too slow to work its way through the system into consumers’ pockets, economists add. A payroll tax holiday would also be less stimulative than a one-time payment, say, in the form of a direct, lump-sum check.

From University of Michigan economist Justin Wolfers:

And Nobel Prize-winning economist Richard Thaler:

To be sure, the fact that key lawmakers are at best skeptical of a payroll tax cut doesn’t render it dead yet. “This is the type of situation where the tree gets bigger,” one top Democratic aide tells me. “We’ll use it to trade for the stuff we want.”

The resistance to the Trump administration’s leading ask does, however, point to a longer timeline for getting a package to the president’s desk. Lawmakers are set to head back to their districts for a week-long recess next week, delaying action until late March at the earliest.

Congressional Democrats are working on their own plan. Senate Minority Leader Chuck Schumer (D-N.Y.) has outlined their priorities:

Providing paid leave for workers who need to weather the virus outbreak at home may offer the readiest point of agreement between the administration and congressional Democrats. Vice President Pence said Trump wants to ensure “hourly workers — hard-working, blue-collar Americans that may not have paid family leave today — that small- and medium-sized businesses in America would be afforded the resources to provide paid leave so that no one would feel that they have to go to work if they might be infected or if they might have been exposed to the coronavirus.”

The White House is also considering targeted relief for certain industries. Among them:

— Oil and natural gas producers. “White House officials are alarmed at the prospect that numerous shale companies, many of them deep in debt, could be driven out of business if the downturn in oil prices turns into a prolonged crisis for the industry,” my colleagues report. “The federal assistance is likely to take the form of low-interest government loans to the shale companies, whose lines of credit to major financial institutions have been choked off, three people said.”

— Airlines, cruise companies, and hotels. Trump “is also seeking to help airlines, cruise companies and hotels, though he has not said how he would do that or pay for it,” per the Post’s reporting. “During the meeting with GOP senators, Mnuchin emphasized that Congress needed to act to help the airline industry in particular.”

— Banks. Top executives from Wall Street’s biggest banks — including Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, and Wells Fargo — are set to meet with Trump today at the White House. The industry has been pushing for long-sought regulatory rollbacks in the face of the crisis, arguing they will ease lending and cushion the blow of the incoming economic shock.

Policymakers’ first, fitful steps toward mustering a fiscal response cheered investors, as the S&P 500 rallied 4.9 percent Tuesday to recover some of its recent losses. But U.S. stock futures tied to major indexes are down roughly 2 percent this morning, pointing to a selloff at the start of the trading session.

And at least one financial advisory firm, Signal Global Advisors, is warning its clients to temper expectations. After a round of meetings with lawmakers on the Hill, the firm “told its associates that lawmakers were ‘behind the curve’ in understanding the impact of the downturn in the market is having on the broader economy,” CNBC’s Brian Schwartz reports, quoting a note from the group.

The firm said it is “pessimistic about the odds of a convincing political fiscal response.”

MARKET MOVERS

Coronavirus response in the United States:

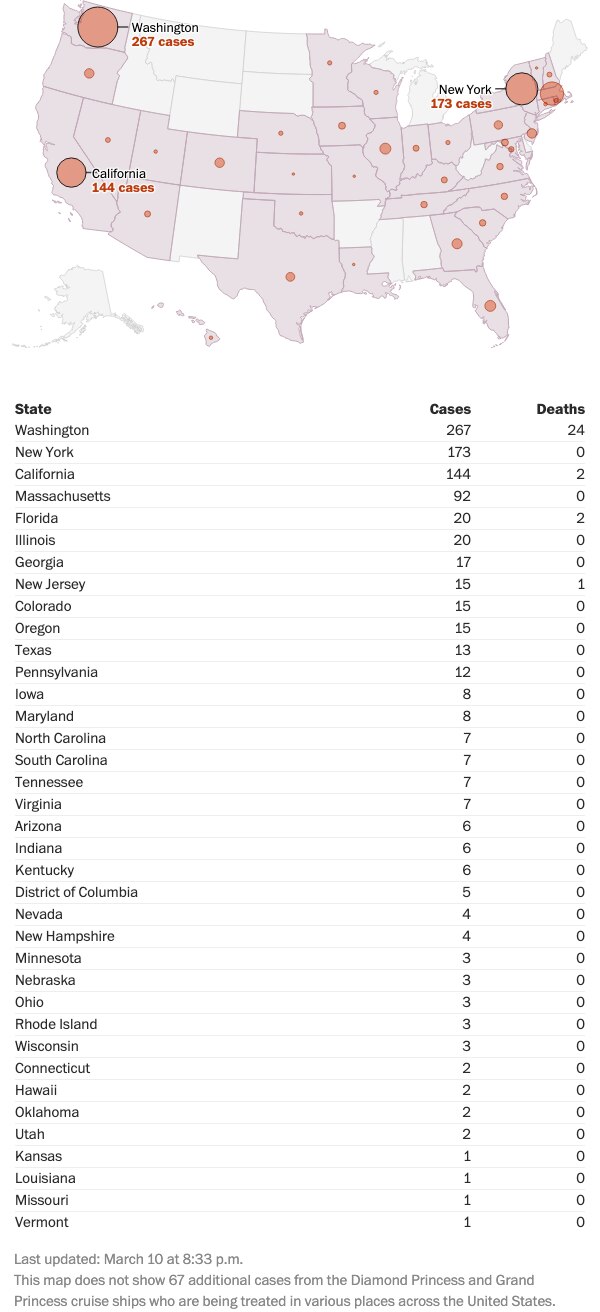

- U.S. cases top 1,000: “There are now more than 1,000 reported cases of covid-19, the disease caused by the virus,” my colleagues Adam Taylor and Teo Armus report. “A growing list of at least 19 states have declared a state of emergency, including on Tuesday Colorado, North Carolina and Michigan, the latter of which reported its first two cases.”

(Graphic by Post staff)

- Trump administration wants federal workers to work from home: “[The] administration is racing to develop contingency plans that would allow hundreds of thousands of employees to work remotely full time, an extreme scenario to limit the coronavirus that would test whether the government can carry out its mission from home offices and kitchen tables,” my colleague Lisa Rein reports.

- A New York suburb is effectively on lock down: “New York Gov. Andrew M. Cuomo took the country’s most drastic steps to curb the spread of the coronavirus , ordering the closure of schools and other gathering places within a one-mile radius in this New York suburb. The creation of what he called a ‘containment zone’ for two weeks will keep about half the city’s 10,500 students at home and will allow the National Guard to sanitize public spaces,” my colleagues Ben Guarino, Sarah Pulliam Bailey, Laura Meckler and Katie Zezima report from New Rochelle, N.Y., a city of 79,000 people.

- Top regulators talk market resilience: “Top U.S. financial regulatory officials including Federal Reserve Chairman Jerome Powell and [Mnuchin] discussed the resilience of financial markets amid the spread of coronavirus on Tuesday,” Reuters’s Pete Schroeder reports. “The Treasury also announced that the Financial Stability Oversight Council, another regulatory panel, will hold an open meeting March 23 to discuss similar issues.”

- Coronavirus conference canceled because of the coronavirus: The Council on Foreign Relations scrapped the event, titled “Doing Business Under Coronavirus,” that was set for Friday in New York, Bloomberg reports. It’s one of a long list of gatherings in the city that have been scotched or rescheduled for later in the year.

Corporate fallout:

- Airlines continued to be slammed: “The latest updates from Delta, American, United and Southwest airlines signaled just how bleak their outlook is for the months to come,” my colleague Rachel Siegel reports.

- Major companies overhaul sick leave policies: “Companies such as Walmart, Uber and Apple are among those announcing new policies that they say are designed to keep employees and customers safe from the coronavirus. Here is a look at major employers that have so far adapted their leave policies,” my colleague Abha Bhattarai reports. “ And as travelers cancel vacations, businesses discourage employees from leaving town, and conventions are canceled en mass, industry executives are comparing the outbreak’s fear factor to the aftermath of the Sept. 11, 2001, terrorist attacks.”

International fallout:

- China tries to repair its supply chains: “Leader Xi Jinping may have signaled victory over the virus, but things are still far from normal here. Factories in the ‘manufacturing hub of the world’ are struggling to get up to full speed. Supply chains have been severely disrupted because parts are not being made and transportation networks have ground to a halt,” my colleague Anna Fifield reports from Beijing. “Together, all this raises the prospect that the coronavirus epidemic will do what the trade war did not: prompt American companies to lessen their reliance on China.”

- Bank of England cuts rates: “The Bank of England announced that it would cut interest rates by from 0.75 percent to 0.25 percent, a record low for Britain’s central bank and one part of a series of measures designed to promote economic activity amid the novel coronavirus,” my colleague Adam Taylor reports. “The cut is the first since August 2016, when it was briefly cut to 0.25 before being raised back to 0.50 percent in November of that year.”

- Saudi Arabia to boost oil production: “Saudi Arabia fired another salvo in its oil-market war with Russia on Wednesday, unveiling plans to boost its oil-production capacity to a record 13 million barrels a day. The price of crude oil fell more than 3% after the announcement,” the WSJ reports.

2020 WATCH

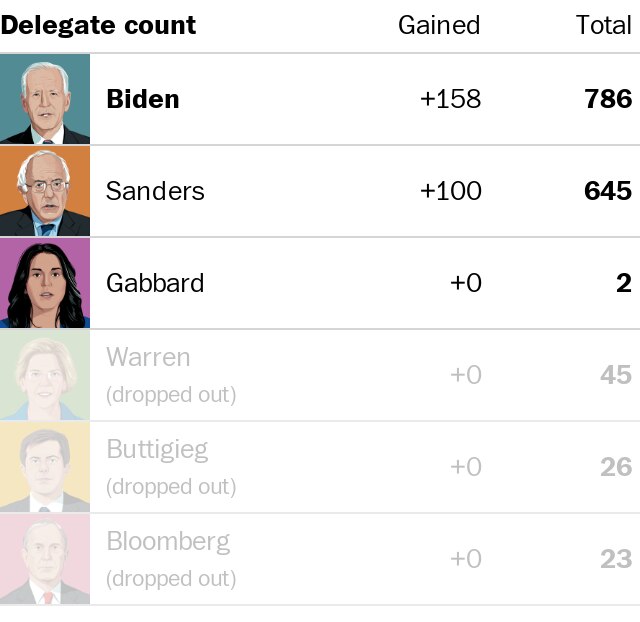

— Biden keeps winning, including Michigan: “Former vice president Joe Biden seized control of the Democratic presidential contest Tuesday with four victories, including a decisive win in Michigan that struck a devastating blow to Bernie Sanders’s ambitions after the senator from Vermont committed his campaign to winning the key Midwestern swing state,” my colleagues Sean Sullivan, Matt Viser and Michael Scherer report.

“Biden also scored resounding wins Tuesday in Mississippi, Missouri and Idaho while two other states — North Dakota and Washington — continued to count ballots. The results showed further evidence of the powerful coalition that Biden has assembled to fuel his remarkable turnaround in the past few weeks, particularly black voters who form the backbone of the Democratic Party and the suburban women who helped drive record turnout for Democrats in the 2018 elections.”

The former veep is on his way to the nomination: “Biden remains well short of the 1,991 pledged delegates needed for a first-ballot victory at the national convention in Milwaukee in July. But with Tuesday’s results, he has solidified his lead in the delegate battle and, with the states that will hold their primaries in the next two weeks, that advantage inevitably will grow,” my colleague Dan Balz writes.

Here’s the current delegate count: (Note: Many delegates are still being allocated,)

(Graphic by Terri Rupar, Ashlyn Still and Reuben Fischer-Baum/The Post)

— Democratic super PAC lines up behind Biden: “Priorities USA, among the largest Democratic political action committees, said it was preparing to expend resources backing Biden, effectively counting on his emergence as the party’s nominee,” my colleague Isaac Stanley-Becker reports.

“The announcement offered further illustration of how the machinery of the Democratic Party and allied groups is falling into place behind Biden.”

- Another group plans to put up ads in swing states: “Democratic group American Bridge said that it plans to support Biden, and will launch a $2.2 million ad buy in Pennsylvania on Wednesday to help Biden’s chances in the general election,” my colleague Michelle Lee reports.

POCKET CHANGE

Wells Fargo CEO and President Charles Scharf. (Alex Brandon/AP)

— New Wells Fargo CEO says bank’s culture was “broken”: “Wells Fargo has suffered from a broken culture and failed leadership but can turn itself around, its new CEO told lawmakers, in the bank’s latest pitch to emerge from years of scandal and controversy,” my colleague Renae Merle reports.

“Charles Scharf is the third Wells Fargo chief executive in three years to try to convince Congress that he can turn around the troubled bank. Rep. Maxine Waters (D-Calif.), chair of the House Financial Services Committee, started the hearing by telling Scharf, who started in October, that the two CEOs who preceded him resigned shortly after testifying, eliciting laughs in the room.”

- Scharf’s bid to repair Wells’s image faces an uphill climb: Last week, “the Financial Services Committee released a more than 100-page report that found the bank repeatedly failed to live up to regulators’ demands that it repay consumers and didn’t aggressively address its cultural problems, despite public promises. Two of the bank’s board members resigned Sunday after the report showed they had resisted becoming involved in addressing Wells Fargo’s problems.”

- Waters also called for an investigation into comments by one of the former executives: She “asked the Justice Department to investigate statements former Wells Fargo CEO Tim Sloan made to the committee last year, which the committee report called ‘inaccurate and misleading.’” (Sloan’s attorney denied those allegations in a statement.)

Scharf eked out a win, in the judgment of CapAlpha’s Ian Katz. “When a CEO sits in front of an angry congressional committee, the result has to be considered a success for the company if it isn’t an obvious failure,” he writes. “So with that low bar, the hearing was a success for Wells Fargo.”

— Goldman is open to acquisitions: Goldman Sachs Group Inc Chief Financial Officer Stephen Scherr said “the bank is ‘very open’ to acquisitions, especially those that would speed the growth of its existing businesses,” Reuters’s Elizabeth Dilts Marshall reports.

“There has been wide investor speculation about Goldman’s appetite and ability to do mergers or acquisitions since rival Wall Street bank Morgan Stanley announced plans last month to buy discount broker E*Trade.”

WSJ News Exclusive | PepsiCo Nears Deal to Buy Energy-Drink Maker

The beverage giant would pay $3.85 billion for Rockstar Energy Beverages under a deal being discussed.

WSJ

CHART TOPPER

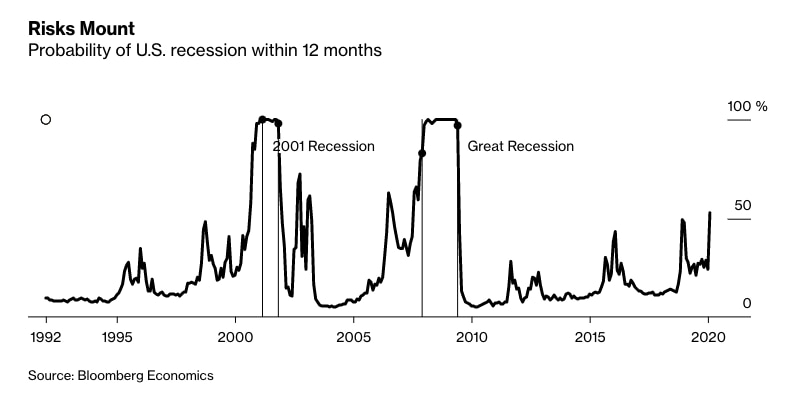

— Recession risk is spiking. Bloomberg Economics’ recession tracker now places the odds of one in the next 12 months at 53 percent. That’s the highest such reading since June 2009 and more than twice the reading just last month:

DAYBOOK

Today:

- Trump meets with bankers about the coronavirus response

- The Financial Services Subcommittee on National Security, International Development, and Monetary Policy holds a hearing about how financial systems “facilitate the illicit trade in people, animals, drugs and weapons”

Thursday:

- Dollar General, Gap, Tupperware, Slack Technologies, Broadcom and Adobe are among the notable companies to report their earnings

Friday:

- The University of Michigan releases a preliminary report on consumer sentiment for March